ECL Calculation for Islamic Banks

The transition from “incurred loss” to “expected credit loss” (ECL) has been a transformative shift for the global financial landscape. For Islamic financial institutions (IFIs), this transition involves navigating the standard requirements of IFRS 9 (Financial Instruments) while often adhering to the Shari’ah-compliant frameworks set by AAOIFI (Accounting and Auditing Organization for Islamic Financial Institutions), specifically FAS 30.

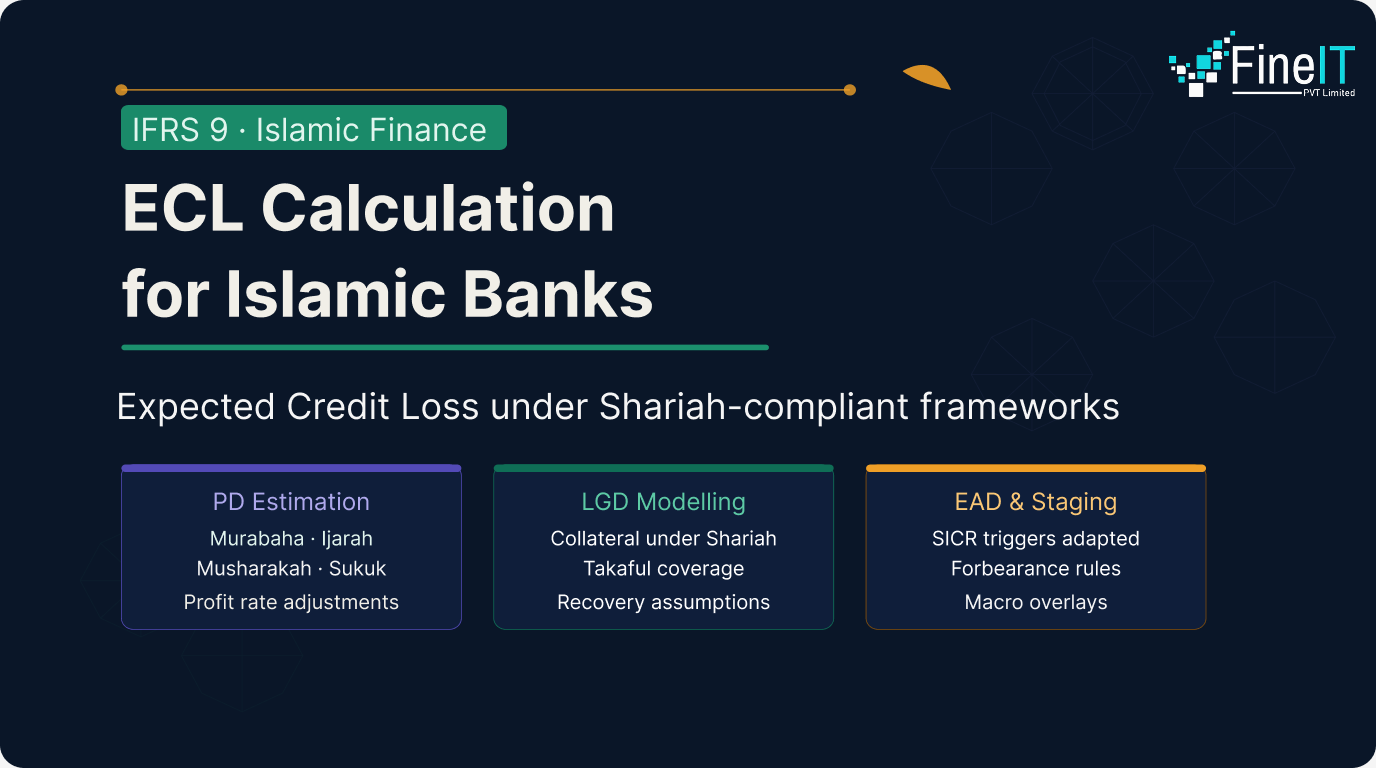

1. What are the core components of ECL?

The ECL model is forward-looking, requiring banks to recognize potential losses before a default event occurs. The calculation generally follows the formula:

$$ECL = PD \times LGD \times EAD$$

Probability of Default (PD):

The likelihood that a counterparty will fail to meet its obligations within a specific timeframe.

Loss Given Default (LGD):

The share of the exposure the bank expects to lose if a default occurs, after considering collateral.

Exposure at Default (EAD):

The total amount to which the bank is exposed at the time of default.

2. How does the three-stage impairment model work?

Both IFRS 9 and FAS 30 typically utilize a “building block” approach, categorizing financial assets into three stages based on the change in credit risk since initial recognition:

| Stage | Credit Risk Status | ECL Requirement |

| Stage 1 | Performing (No significant increase in risk) | 12-month ECL |

| Stage 2 | Under-performing (Significant increase in risk – SICR) | Lifetime ECL |

| Stage 3 | Non-performing (Credit-impaired/Default) | Lifetime ECL |

3. What unique challenges do Islamic banks face?

While the mathematical framework is similar to conventional banking, the nature of Shari’ah-compliant contracts introduces several unique modeling complexities:

How do Murabaha contracts differ from conventional loans?

In a conventional bank, a loan is an interest-bearing instrument. In an Islamic bank, a Murabaha is a cost-plus-profit sale. Because the profit is “locked in” at the start as part of the purchase price, the “effective interest rate” (EIR) used for discounting in IFRS 9 must be carefully mapped to the Expected Profit Rate.

How does asset ownership function in Ijarah?

In Ijarah (leasing) contracts, the bank often retains legal ownership of the underlying asset. This impacts the LGD calculation, as the recovery process involves repossessing and selling a tangible asset rather than just claiming a debt.

C. Profit and Loss Sharing (Mudarabah & Musharakah)

These contracts involve equity-like risks. Defining a “credit loss” in a partnership where the bank shares in the loss is philosophically different from a default on a fixed-income product. Models must distinguish between a business failure (shared loss) and a breach of contract by the partner (credit event).

What are the implications of late payment charges?

Shari’ah principles generally prohibit banks from keeping “penalty interest” as income (it is usually donated to charity). This affects the EAD and cash flow projections, as the bank cannot accrue compounding interest on defaulted amounts.

4. How do AAOIFI FAS 30 and IFRS 9 compare?

While many Islamic banks in regions like the UAE or Malaysia follow IFRS 9, others—particularly in Bahrain or Qatar—may follow AAOIFI FAS 30.

- FAS 30 (Impairment, Credit Losses and Onerous Commitments) was designed specifically to align ECL logic with Shari’ah requirements.

- It places a heavy emphasis on the economic substance of Islamic contracts and provides more tailored guidance on how to treat “Onerous Commitments” in Shari’ah-compliant trade finance.

5. What is the future outlook for data and macro-scenarios?

The “forward-looking” requirement of ECL means banks must integrate macroeconomic variables (GDP growth, oil prices, inflation) into their models. For Islamic banks, this requires sophisticated Scenario Analysis—often involving “Base,” “Optimistic,” and “Pessimistic” views—to ensure that the provisions held today are sufficient for the economic realities of tomorrow.

Ready to simplify ECL for Islamic banking?

With FineIT, seamlessly align IFRS 9 and AAOIFI FAS 30 while tackling complex Shari’ah-compliant contracts—powered by intelligent automation, precise modeling, and audit-ready insights.

Transform your ECL framework today with FineIT — where compliance meets clarity.

Frequently Asked Questions

About FineIT Private Limited

FineIT Private Limited is a leading Fintech provider.

Published by

Muzammal Rahim

FineIT Private Limited — IASB quantitative advisor, BCBS member institution (est. 2001)