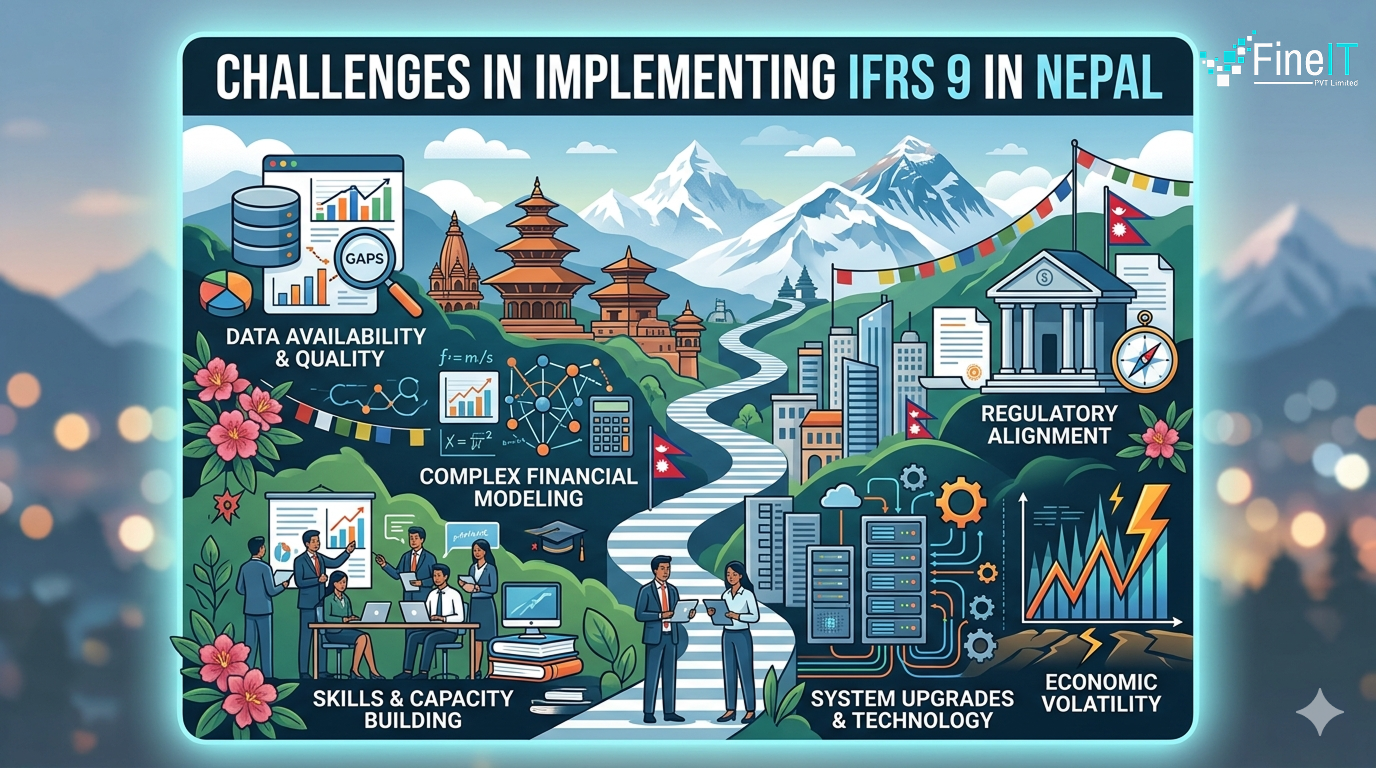

Challenges in Implementing IFRS 9 in Nepal

The transition to NFRS 9 (the Nepal Financial Reporting Standard aligned with IFRS 9) represents a seismic shift for the Nepalese banking sector. While the Nepal Rastra Bank (NRB) initially planned for earlier adoption, the full implementation of the Expected Credit Loss (ECL) model was deferred to the 2081/82 fiscal year (starting mid-July 2024) to allow institutions more time to navigate technical and economic hurdles.

1. What are the challenges with data availability and quality?

The move from an “incurred loss” model to an “expected loss” model requires vast amounts of historical data to calculate the Probability of Default (PD) and Loss Given Default (LGD).

What historical gaps exist in IFRS 9 implementation?:

Many banks in Nepal lack the decade-long, granular data needed to build robust predictive models.

What segmentation issues arise during implementation?:

Segmenting portfolios by risk characteristics (e.g., agriculture, hydropower, and SME loans) is difficult when historical records are inconsistent.

2. Complex Financial Modeling & “Forward-Looking” Requirements

IFRS 9 requires banks to incorporate forward-looking information (FLI) into their risk assessments.

How does macro-economic volatility affect IFRS 9 compliance?:

Nepal’s economy is heavily influenced by remittances, tourism, and agriculture. Integrating these volatile variables into a stable ECL model is a significant technical challenge.

Why is scenario analysis critical for IFRS 9?:

Banks must now develop multiple economic scenarios (Optimistic, Base, and Pessimistic) and assign probability weights to them—a process that is entirely new to many local risk departments.

3. Regulatory Alignment & What carve-outs are available under IFRS 9?

There has historically been a conflict between NRB Unified Directives and NFRS standards.

The “Higher of” Rule:

The NRB often requires banks to maintain a regulatory “backstop.” If the loan loss provision calculated under NFRS 9 is lower than the NRB’s directive-based provision, banks must often hold the higher amount.

Carve-outs:

The Institute of Chartered Accountants of Nepal (ICAN) has issued various carve-outs (valid through 2082/83) to manage the impact on Effective Interest Rate (EIR) calculations and impairment, acknowledging that full compliance is currently “impracticable” for some.

4. What technical expertise and human resources are needed for successful implementation?

There is a significant shortage of professionals who are experts in both the accounting requirements of IFRS 9 and the statistical modeling required for ECL.

How significant is the training gap in IFRS 9 implementation?:

Implementing these standards requires coordination between CFOs, CROs (Chief Risk Officers), and CITOs (Chief IT Officers).

What is the cost of implementing IFRS 9?:

The cost of hiring international consultants, upgrading IT systems to handle automated ECL runs, and training internal staff is a heavy burden for smaller Class B and C financial institutions.

5. What is the impact on capital adequacy?

The shift to ECL generally leads to an increase in impairment allowances, as losses are recognized earlier than under the old system.

How does IFRS 9 create profitability pressure?:

Higher provisions directly impact a bank’s bottom line.

What impact does IFRS 9 have on capital buffers?:

For banks already operating near their minimum capital adequacy ratios, the day-one impact of NFRS 9 could necessitate capital injections or a reduction in dividend payouts.

What are the key takeaways and conclusions?

While the implementation of IFRS 9 will ultimately uplift Nepalese banking to international standards and improve transparency, the journey is fraught with operational and technical hurdles. Success depends on the continued collaboration between the NRB, ICAN, and the Nepal Bankers’ Association (NBA) to ensure that the transition remains stable.

As Nepal’s banking sector advances toward full NFRS 9 / IFRS 9 compliance, institutions need the right mix of data, technology, and risk expertise to successfully implement the Expected Credit Loss (ECL) framework.

At FineIT Solutions, we help financial institutions in Nepal simplify IFRS 9 implementation through advanced ECL modeling, data integration, regulatory alignment, and automated reporting solutions tailored to the local banking landscape.

Looking to accelerate your IFRS 9 journey in Nepal? Connect with FineIT to build a compliant, scalable, and future-ready risk framework.

Frequently Asked Questions

About FineIT Private Limited

FineIT Private Limited is a leading Fintech provider.

Published by

Muzammal Rahim

FineIT Private Limited — IASB quantitative advisor, BCBS member institution (est. 2001)